How Governments and Auditors Define the Ethical Operating Floor for Business

The art of governance is not the accumulation of regulation for its own sake. It is the deliberate construction of standards that protect people, preserve the environment, and ensure that every entity operating within a nation’s borders contributes honestly and proportionately to the common good.

Why Governments Must Own the Reference Table

When companies define their own ethical frameworks in isolation, they do so from a position of self-interest. The frameworks they build may be genuine in aspiration, yet structurally incomplete in consequence. No private organisation has the mandate, the reach, or the enforcement authority to define what fair conduct looks like across an entire national economy. That mandate belongs to government.

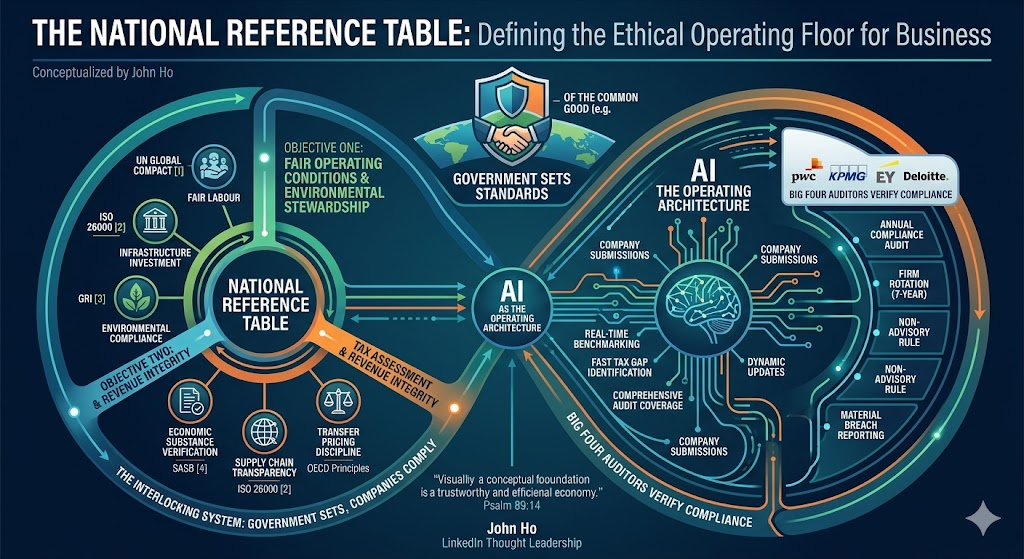

The National Reference Table is the instrument through which a sovereign government sets the non-negotiable operating conditions for every company wishing to conduct business within its jurisdiction. It is not a request. It is not a set of aspirational guidelines. It is the ethical and legal floor of market participation, carrying the full weight of legislative authority, regulatory enforcement, and where necessary, the power of exclusion.

This article examines the National Reference Table from two perspectives that must work in concert: the government that establishes and enforces the standards, and the professional audit firms whose independence and technical rigour are essential to verifying that those standards are genuinely met.

Objective One: Fair Operating Conditions and Environmental Stewardship

The first objective of the National Reference Table is to ensure that every company operating within the country does so fairly toward its workers, its communities, and its natural environment. This is not charity. It is the precondition of a functioning and trusted economy.

Fair Labour Standards

The Reference Table requires that every company pay its employees a living wage indexed to actual cost of living in the regions where those employees work not merely the statutory minimum, which frequently lags economic reality by years. It also requires timely payment, safe working conditions, freedom from discrimination, and access to grievance mechanisms that are structurally protected from employer retaliation. These standards are anchored in the Ten Principles of the UN Global Compact [1], which establish labour rights, human rights, and anti-corruption as the foundational obligations of responsible business. These are non-negotiable. A company that cannot meet them does not meet the threshold for operating in this country.

Infrastructure and Community Investment

Companies whose operations depend on national infrastructure whether roads, ports, utilities, digital networks, or the skilled workforce produced by public education systems carry a reciprocal obligation to contribute to the maintenance and development of that infrastructure. The Reference Table establishes sector-specific investment thresholds calibrated to the scale of infrastructure dependency. The WBCSD’s framework on Corporate Performance and Accountability [5] provides useful architecture for how these obligations can be defined, measured, and disclosed in a way that is meaningful to both government and civil society. The thresholds are transparent, publicly published, and applied uniformly.

Environmental Compliance

The Reference Table establishes emissions ceilings, waste disposal standards, and environmental impact assessment requirements that represent genuine stewardship obligations, not the permissive minimums that industry lobbying has historically produced. Companies are required to demonstrate compliance through independently verified environmental accounts submitted annually and reported against the GRI Standards [3], the globally recognised baseline for sustainability reporting. Pollution is not an externality to be priced. It is a harm to be prevented. The Reference Table makes this explicit in enforceable standards with graduated financial penalties and, for serial violators, operating licence revocation.

Table 1 — National Reference Table: Objective One Standards

| Standard Area | Requirement | Enforcement Mechanism |

|---|---|---|

| Fair Labour | Living wage indexed to regional cost of living; safe conditions; protected grievance access (UN Global Compact [1]) | Annual labour audit; operating licence review |

| Infrastructure Investment | Sector-calibrated investment thresholds proportionate to infrastructure dependency (WBCSD [5]) | Annual infrastructure levy assessment |

| Environmental Compliance | Verified emissions ceilings; waste standards; GRI-aligned impact assessments [3] | Graduated financial penalties; licence revocation for serial non-compliance |

| Community Obligations | Disclosure of community economic footprint; local employment targets where applicable (ISO 26000 [2]) | Public reporting requirement; regulatory review |

Objective Two: Tax Assessment and Revenue Integrity

The second objective of the National Reference Table is fiscal. Every company operating within the country generates economic activity. That activity creates obligations to the public systems that made it possible. The Reference Table grounds tax assessment in verified operational reality rather than in self-reported figures that have historically provided structural opportunity for understatement.

The Reference Table establishes three Tax Assessment Pillars:

Pillar One: Economic Substance Verification

A company’s declared revenues, operating costs, transfer pricing arrangements, and intercompany transactions are benchmarked against independently verified Reference Table metrics for their sector. Sector-specific materiality thresholds are drawn from the SASB Standards [4], which provide industry-calibrated sustainability accounting metrics that translate directly into plausible economic substance benchmarks. Where declared figures fall outside the plausible range, the burden of explanation shifts to the company. Economic activity generates tax liability. The Reference Table ensures that the assessed liability reflects the genuine scale of that activity.

Pillar Two: Supply Chain Transparency

Companies are required to disclose the full economic map of their supply chain within the jurisdiction, including intercompany pricing, royalty arrangements, and the allocation of intellectual property income. The Reference Table establishes sector-specific benchmarks for reasonable supply chain cost structures, informed by the ISO 26000 guidance on organisational governance and fair operating practices [2]. Arrangements that deviate significantly without credible commercial explanation are flagged for detailed assessment review.

Pillar Three: Transfer Pricing Discipline

The Reference Table incorporates the OECD’s arm’s length principles as a national binding standard. Companies with cross-border related-party transactions are required to file contemporaneous documentation demonstrating that their pricing reflects what genuinely independent parties would agree in comparable circumstances. The Reference Table gives tax assessors an explicit sector-calibrated benchmark against which to test that documentation.

Table 2 — National Reference Table: Objective Two Tax Assessment Pillars

| Tax Assessment Pillar | Standard Applied | Auditor Verification Requirement |

|---|---|---|

| Economic Substance Verification | Declared revenues benchmarked against SASB sector Reference Table metrics [4] | Independent audit of economic substance accounts |

| Supply Chain Transparency | Full intercompany pricing and IP income disclosure; ISO 26000 fair operating practices [2] | Verified supply chain economic map filed annually |

| Transfer Pricing Discipline | OECD arm’s length principles as binding national standard | Contemporaneous TP documentation reviewed by auditor |

AI as the Architecture That Makes This Feasible

A framework of this breadth spanning fair labour, environmental stewardship, supply chain transparency, and transfer pricing discipline across every qualifying company in a national economy would have been administratively impossible to operate at scale even a decade ago. The volume of data, the speed of cross-referencing, and the analytical depth required to benchmark thousands of company submissions against sector-calibrated standards simultaneously would have overwhelmed any conceivable team of human reviewers. Artificial intelligence has changed that calculus entirely.

AI large language models can ingest a company’s full Reference Table submission and benchmark it against the GRI Standards [3], the UN Global Compact Principles [1], ISO 26000 guidance [2], and sector-specific SASB Standards [4] in minutes, surfacing gaps, anomalies, and deviations that manual review would take weeks to identify. For tax assessors, AI can cross-reference declared economic substance figures against sector benchmarks drawn from the WBCSD’s corporate performance framework [5], flagging outliers for human investigation with a speed and consistency that rule-based systems alone cannot match.

For PwC, KPMG, EY, and Deloitte, AI transforms the compliance audit from a sampling exercise into a comprehensive review. Rather than testing a representative selection of transactions and extrapolating, AI-assisted audit tools can examine entire transaction populations, identifying patterns of deviation that selective sampling would statistically miss. This does not replace auditor judgement. It sharpens it directing experienced professionals toward the areas where judgement is most needed and most consequential.

For government, AI enables real-time monitoring of aggregate compliance across the national economy. Regulators can identify sectors where Reference Table compliance is deteriorating before individual company breaches accumulate into systemic failures. They can calibrate enforcement resources toward the highest-risk areas rather than distributing them uniformly across low and high-risk companies alike. And they can update sector benchmarks dynamically as economic conditions change, ensuring the Reference Table remains a living standard rather than a fixed document that industry learns to work around.

The National Reference Table is not a bureaucratic exercise. With AI as its operating engine, it becomes a genuinely intelligent accountability system, one that is proportionate, adaptive, and capable of maintaining the rigour that the public interest requires at a scale that no purely human system could sustain.

Table 3 — AI Capabilities in the National Reference Table Architecture

| Actor | AI Capability | Outcome |

|---|---|---|

| Government Regulators | Real-time benchmarking of company submissions against GRI [3], SASB [4], UN Global Compact [1] | Early detection of sectoral non-compliance trends |

| Tax Assessors | Cross-reference declared substance figures against WBCSD sector benchmarks [5]; flag transfer pricing outliers | Faster, more consistent tax gap identification |

| Big Four Auditors | AI-assisted full-population transaction review; anomaly detection across Reference Table pillars | Sampling replaced by comprehensive audit coverage |

| Companies | AI-assisted self-assessment against ISO 26000 [2] and SASB [4] before submission | Reduced compliance cost; stronger audit readiness |

The Role of the Big Four: PwC, KPMG, EY, and Deloitte

Government can set the Reference Table. It cannot audit every company in the country. That is where the professional audit firms PwC, KPMG, EY, and Deloitte carry a responsibility that goes beyond their commercial mandate. In the National Reference Table framework, these firms are not merely the company’s agents. They are verifiers of compliance with national standards, operating under a duty of care that runs not only to their audit client but to the public interest the Reference Table was designed to protect.

Reference Table Compliance Audits

Every company above the prescribed revenue threshold is required to commission an annual Reference Table Compliance Audit from a qualified independent auditor. The audit has three components: verification of fair labour and community investment obligations, verification of environmental compliance accounts reported against the GRI Standards [3], and verification of the economic substance and transfer pricing documentation underpinning the tax assessment pillars.

Auditor Independence and Rotation

The Reference Table requires mandatory audit firm rotation every seven years for all companies above the threshold. It prohibits audit firms from providing tax advisory or transfer pricing services to companies they audit, a structural conflict of interest that has historically compromised the independence that public confidence in audit requires.

Reporting Obligations

Where a Reference Table Compliance Audit identifies material non-compliance, the auditor is required to report the finding to the relevant government authority within thirty days of issuing the audit opinion. The auditor’s duty of confidentiality to its client does not extend to concealment of material breaches of national operating standards. This reporting obligation is the structural mechanism that ensures the audit profession functions as a genuine line of public defence and not merely as a commercial certification service.

Table 4 — Auditor Responsibilities Under the National Reference Table

| Auditor Obligation | Scope | Public Interest Dimension |

|---|---|---|

| Annual Compliance Audit | Labour, environmental (GRI [3]), tax assessment pillars | Independent verification for government and public |

| Firm Rotation (7-year) | Mandatory across all threshold companies | Prevents capture; preserves independence |

| Non-Advisory Rule | No tax or TP advisory to audit clients | Eliminates structural conflict of interest |

| Material Breach Reporting | Report to government within 30 days of audit opinion | Auditor as line of public defence, not client shield |

The Interlocking System: Government Sets, Auditors Verify, Companies Comply

The National Reference Table creates an interlocking three-party accountability system. Government sets the standards, anchored in the UN Global Compact [1], ISO 26000 [2], GRI [3], SASB [4], and WBCSD [5] publishes them transparently, and enforces them with genuine consequence. Audit firms verify compliance independently, reporting breaches to public authorities where required. Companies operate within the framework as the price of market access, with the understanding that the standards are applied uniformly, that compliance confers genuine competitive credibility, and that non-compliance carries consequences that make evasion economically irrational.

AI makes this system operable at national scale. Without it, the Reference Table risks becoming what so many compliance frameworks before it have become a document of declared intention whose verification is too resource-intensive to be genuinely comprehensive. With AI as its operating architecture, the National Reference Table becomes an active, responsive, and enforceable standard that is proportionate to the complexity of the modern economy it governs.

The difference between aspiration and obligation is enforceability. The National Reference Table grounded in global standards, operated by AI, and verified by independent auditors converts the former into the latter. In doing so, it does not constrain the economy. It protects the foundation on which a genuinely sustainable economy is built.

Key References

[1] UN Global Compact — Ten Principles of Responsible Business:

[2] ISO 26000 — Guidance on Social Responsibility:

[3] GRI Standards — Global Baseline for Sustainability Reporting:

[4] SASB Standards — Sector-Specific Sustainability Accounting (IFRS Foundation):

[5] WBCSD — Corporate Performance and Accountability:

Important Disclaimer — Please Read

This article was developed with AI assistance and represents the original thought leadership and proprietary frameworks of John Ho. The National Reference Table concept, as presented herein, is the intellectual property of John Ho. References to PwC, KPMG, EY, Deloitte, GRI, OECD, ISO 26000, UN Global Compact, SASB, and WBCSD are used for illustrative and educational purposes only. No endorsement by or affiliation with those organisations is implied. All referenced URLs were accurate at the time of writing; the author accepts no responsibility for subsequent changes. This article is for thought leadership and educational purposes only and does not constitute legal, tax, regulatory, or financial advice.

Image Disclaimer: This visual infographic was conceptualized and generated by Gemini (Google AI) based on the “National Reference Table” thought leadership article by John Ho. It is intended for illustrative and educational purposes to visually map out the interlocking framework of governance, AI-driven auditing, and corporate compliance. All logos, standards, and regulatory frameworks mentioned are the property of their respective trademark holders.

This article was written by Dr John Ho, a professor of management research at the World Certification Institute (WCI). He has more than 4 decades of experience in technology and business management and has authored 28 books. Prof Ho holds a doctorate degree in Business Administration from Fairfax University (USA), and an MBA from Brunel University (UK). He is a Fellow of the Association of Chartered Certified Accountants (ACCA) as well as the Chartered Institute of Management Accountants (CIMA, UK). He is also a World Certified Master Professional (WCMP) and a Fellow at the World Certification Institute (FWCI).

ABOUT WORLD CERTIFICATION INSTITUTE (WCI)

World Certification Institute (WCI) is a global certifying and accrediting body that grants credential awards to individuals as well as accredits courses of organizations.

During the late 90s, several business leaders and eminent professors in the developed economies gathered to discuss the impact of globalization on occupational competence. The ad-hoc group met in Vienna and discussed the need to establish a global organization to accredit the skills and experiences of the workforce, so that they can be globally recognized as being competent in a specified field. A Task Group was formed in October 1999 and comprised eminent professors from the United States, United Kingdom, Germany, France, Canada, Australia, Spain, Netherlands, Sweden, and Singapore.

World Certification Institute (WCI) was officially established at the start of the new millennium and was first registered in the United States in 2003. Today, its professional activities are coordinated through Authorized and Accredited Centers in America, Europe, Asia, Oceania and Africa.

For more information about the world body, please visit website at https://worldcertification.org.